Why we think Sandisk is a downgrade rating to a sell

What if SanDisk is closer to the semiconductor peak cycle than the market currently thinks?

That is the key risk investors need to consider when thinking about joining the euphoria AI memory trade.

Memory cycles inherently have a long history of hurting investors when expectations become too stretched. In 2018 and 2022, the NAND flash cycle turned sharply, and pricing weakness flowed quickly through earnings and share prices. In 2018–2019, NAND flash prices fell around 23% YoY, leaving investors exposed to a brutal cyclical correction

If a similar downturn emerged today, SanDisk’s share price would likely fall hard.

However, that is not the exact call we are making just yet because many analysts and investors think “This time is different,” and in many ways it is, but the principles and cyclical nature are very much the same.

In any cycle, whether it is the trough, recovery, peak or decline, there are usually features and characteristics that help investors interpret where we are in the cycle.

The hard part is timing the exact top or bottom. That usually requires a catalyst, and those catalysts are often only obvious in hindsight.

As you will see, we think the more important point is that SanDisk is starting to show late-cycle characteristics. That means the risk/reward is becoming less attractive.

SanDisk 3,300% return has investors shocked

SanDisk has had an extraordinary run, with the stock up more than 3,300% in just over a year. That move has been driven by a powerful combination of tight memory supply, strong data centre demand, pricing power across NAND flash, and the broader AI-driven re-rating across semiconductor names.

This has created a near-perfect earnings backdrop. SNDK Gross margins have surged to 80%, investors have become increasingly confident, and the market has started to price SanDisk as though the current conditions can last for much longer.

But that is where the risk now sits.

Everyone already knows the positive story. The market understands the memory shortage. It understands the AI data centre demand. It understands the pricing power. The problem is that SanDisk’s valuation now appears to be pricing in very little downside risk.

Let’s talk about SanDisk margins

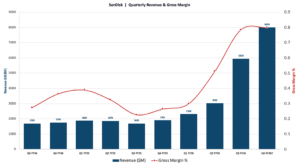

SanDisk’s margin profile shows just how stretched this cycle has become.

In Q3 2024, SanDisk generated US$468m in gross profit at a 27% gross margin. Just two years later, gross profit has surged to US$4.6bn, with gross margins reaching 78.4%.

An 80% gross margin is not a normal or sustainable level for a commodity memory business. Through a more normal cycle, NAND gross margins typically sit closer to 25–35%. At some point, which we expect in CY27, investors should expect margins to come back down. Every percentage point above roughly 45% looks cyclical, not structural.

That is the key message from the chart. Gross margins are still exceptionally high, but the rate of improvement is now starting to slow. The hyperbolic pricing dynamics that drove the memory market over the past two years appear to be stabilising.

For context, during the 2017–2018 memory cycle peak, 40–50% gross margins were already considered extremely strong. SanDisk is now operating well above that range. The reason is Data centre demand has created an unprecedented stretch in NAND pricing.

SanDisk’s data centre revenue has increased 7.4x in just two quarters. But this was not mainly driven by a massive increase in unit volumes. It was driven by price. And because of that price increase, its consumer segment market is now starting to decline.

Because prices are now so high, consumer willingness to buy products like PCs, gaming devices, and other electronics is starting to weaken.

That matters for SanDisk because NAND demand is still tied heavily to consumer devices. If data centre growth also starts to slow, SanDisk could face a double revenue hit.

The first would come from weaker consumer demand. The second would come from softer data centre demand.

At the same time, margins would also come under pressure if NAND pricing begins to normalise. That is the real downside risk. SanDisk could face falling revenue and falling margins at the same time. A massive catalyst for multiple compressions.

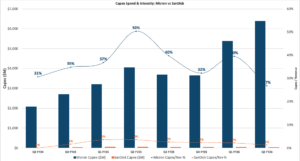

SanDisk is not expanding capacity like in previous cycles

The most interesting part of our analysis is also the most counterintuitive part of the thesis.

At first glance, SanDisk not aggressively building out capacity looks like discipline. In a tight market, that makes sense. Less supply supports pricing, protects margins and helps the company capture the full benefit of the current NAND upcycle.

But that discipline cuts both ways.

SanDisk spent more through the trough and recovery phase, but capex has since remained fairly stable. Micron, by contrast, is spending far more aggressively on new capacity. On our numbers, Micron is investing at roughly 20x the rate of SanDisk on a proportional basis.

That strategy works beautifully on the way up. When supply is tight, SanDisk can sell into a stronger pricing environment without flooding the market with new wafers.

Through the full cycle, however, the winners are usually the companies with the lowest cost per wafer (which requires investment), the deepest customer relationships, and the strongest balance sheets. If SanDisk does not keep investing, it risks falling behind Samsung, SK Hynix and Micron, all of which have new capacity expected to come online across CY27 and CY28 from the capex being spent today.

When that supply hits, the market will look very different.

Every memory cycle has shown the same pattern. The companies with the weakest capex profile near the peak are often the ones whose margins get hit hardest in the trough. Qimonda in 2009. Elpida in 2012. SMIC and Nanya in 2019.

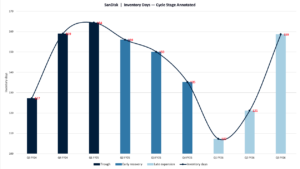

Why is inventory days the cleanest cycle indicator

Inventory is probably the single most important indicator in a memory cycle.

It tells us what is happening to demand before it fully shows up in pricing. Analysts focus on it because it shows how many days of production are sitting on the balance sheet waiting to be sold.

Inventory days usually lead pricing by around two quarters. What we mean is there is a delay between the inventory held on the balance sheet and the pricing of the NAND memory.

When inventory builds, suppliers eventually need to clear it. And when they need to clear it, they usually cut prices.

SanDisk’s inventory days have now increased from 107 days in Q1 FY26 to 159 days in Q3 FY26. That is a 52-day increase in just two quarters.

You can see this clearly in the chart. SanDisk’s inventory is now starting to build back toward trough-cycle levels. If this pace continues, gross margins could begin to pull back over the next two to three quarters.

The next quarter will be important. If inventory remains elevated, it would strengthen the thesis that SanDisk is moving into the later stages of the cycle, where pricing power starts to fade and margin risk begins to rise.