Government cash covers half the drill cost on 130 PJ of mostly uncontracted Cooper Basin gas

Small-cap gas drillers rarely get someone else to pay half the bill. Vintage Energy (ASX:VEN) just did, signing grant agreements with the South Australian government for two A$2.5 million payments tied to drilling Odin-3 and Vali-4 in the Cooper Basin.

The grants were first flagged on 20 February. Today’s news is the actual signed paperwork, with cash expected to land before 30 June 2026. That timing matters because it lets management lock in rig availability and finalise a drilling contract rather than wait on the next capital raise to do it.

For a company sitting on its share of more than 130 PJ of gross proved and probable gas reserves, mostly uncontracted, the constraint has never been the resource. It has been the funding gap between discovery and production. A A$5 million cornerstone from the state government closes a meaningful slice of that gap on two specific wells.

The fields already supply ENGIE and AGL. The question now is whether Odin-3 and Vali-4 deliver enough new flow to convert that relationship into something larger.

Why South Australia is writing the cheque

The SA Gas Incentive Grant program is a A$15 million pot designed to accelerate gas supply, storage and infrastructure ahead of a 30 September 2028 delivery deadline. Vintage and its joint venture partners Metgasco and Bridgeport have just secured a third of it.

The political read is that South Australia is worried about east coast gas supply tightness and is willing to subsidise drilling to fix it. The commercial read is more useful. Government grants signal that an independent assessor looked at the Odin and Vali fields and concluded they are technically and economically sound enough to bet public money on.

That endorsement matters for a company of Vintage’s size. It also lowers the dilution risk on these specific wells, which is exactly the kind of news long-suffering holders have been waiting for.

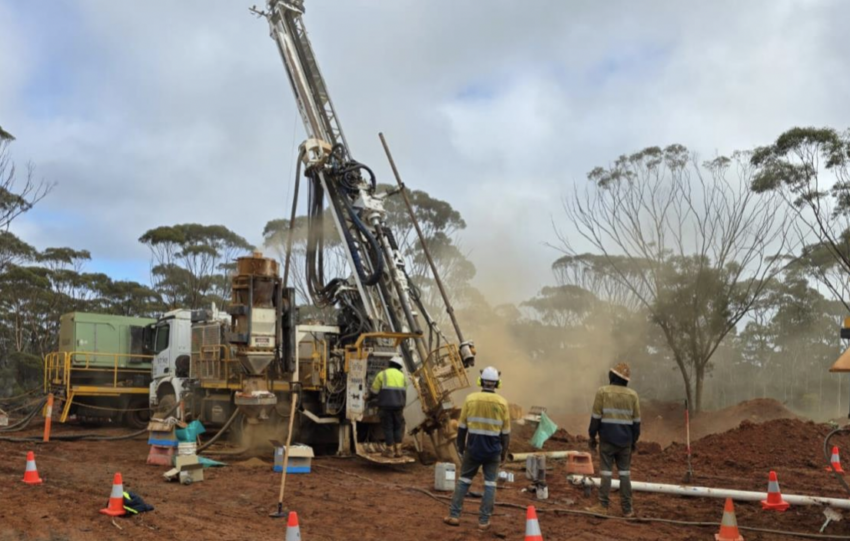

The drilling case rests on a near-perfect track record

Five wells have been drilled across the Southern Flank projects. All five found gas. Vali-1 and Odin-1 were genuine new field discoveries, and the follow-up wells have proven the Toolachee and Epsilon reservoirs as strong producers.

Vali-4 is now targeting fresh access to the Toolachee Formation plus shallower Nappamerri sands identified using AI-assisted seismic interpretation. Odin-3 is essentially a repeat of the Odin-1 setup, which is the lowest-risk geological bet on the program.

We think the more interesting question is not whether the wells find gas. It is whether the connection into the existing Cooper Basin gathering network happens quickly enough to convert reserves into contracted revenue before the 2028 delivery deadline starts pressuring everyone.

What 130 PJ of uncontracted gas could actually be worth

Vintage’s 50% share of more than 130 PJ of gross 2P reserves is the number that matters for the long-term valuation case. East coast gas prices have been structurally elevated, and the majority of that gas is uncontracted and sitting next to existing infrastructure.

The skeptical read is that reserves on paper are not the same as cash in the bank. Vintage has spent years moving from discovery to flowing gas, and small drillers routinely underestimate the time and capital required to ramp production to commercial scale.

The grant does not change the resource. It changes the funding path to monetising it, which has been the bottleneck all along.

Can Odin-3 and Vali-4 turn 130 PJ on paper into contracted revenue?

Grant cash arrives by 30 June 2026, rig contracting follows, and the drilling outcomes of Odin-3 and Vali-4 will reshape the conversation around contracted reserves and offtake renegotiation with ENGIE and AGL.

Investors should watch three things. The actual drill timing once rig availability is confirmed, the flow rates from both wells against the Odin-1 and Vali-1 benchmarks, and any signs of new offtake discussions on the uncontracted portion of the 130 PJ reserve base. For broader macro context on energy and rates that shape this thesis, our recent work at stocksdownunder covers the central bank backdrop that ultimately drives capital costs for drillers like this one.

Get the drilling right and the conversation shifts from grant-funded survival to genuine production growth. Miss, and the funding gap reopens fast.