The rise in demand for electronic devices, particularly electric vehicles, has been a boon for companies such as Pilbara Minerals (ASX: PLS). But how does it fare against the competition?

Pilbara Minerals owns one of the world’s largest lithium mines

Pilbara Minerals’ Pilgangoora project is one of the world’s biggest lithium mines. It lies 120km from Port Hedland and is one of the largest deposits of lithium spodumene and tantalum in the world. Spodumene is the mineral that yields lithium while tantalum is valuable for its use in electronics and alloy metals given its corrosion-resistant properties.

Pilgangoora is a hard rock project, which is costlier to mine than underground brine deposits. But beggars for lithium cannot be choosers. Only hard rock lithium can convert directly to lithium hydroxide – the chemical that might be needed over lithium carbonate to improve energy density in batteries in the years ahead.

The company has remained strong in spite of volatility

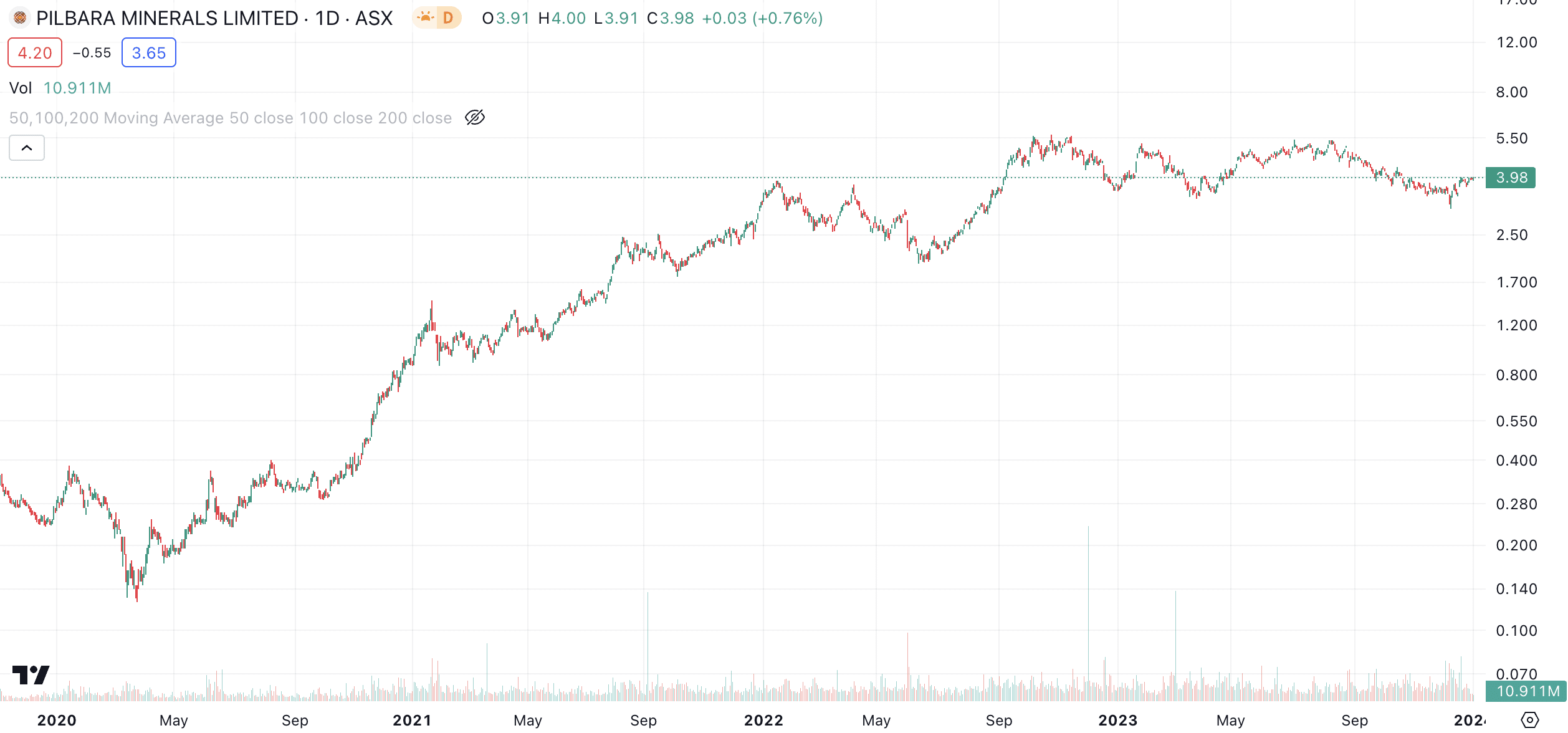

Pilgangoora began commercial production back in April 2019. The first 12 months were tough because of the oversupply in the lithium market and, in early 2020, the Corona Crash. But the share price recovered in conjunction with the lithium price and increased demand for electric vehicles. Governments have made their carbon emission targets clearer, ushering in a new era of electric powered transportation. And the rise of Tesla has led to almost all other car manufacturers scrambling to catch up.

The Asian connection

Pilbara Minerals timed its run perfectly, signing a five-year offtake agreement with Chinese lithium producer Yibin Tianyi back on 25 March 2020. And in October of that year, it bought the Altura Lithium Operations for US$175m, expanding the Pilgangoora operation and leveraging the lithium price recovery. Beyond its lithium resource, the company is building a 6MW solar farm at Pilgangoora and has a joint venture agreement with POSCO to develop a lithium hydroxide conversion facility in South Korea. Pilbara Minerals’ share price has risen from 22 cents two years ago to $2.93 today – a gain of over 1,200%!

A solid FY23 – but is more growth to come?

In FY23, Pilbara Minerals made $4.1bn in revenue, up from $1.2bn just 12 months prior, off the back of 607.5kt in lithium shipped, up 68% from the year before – at an average lithium price of 87% higher than the year before.

The company’s post-tax profit came in at $2.4bn, up from $0.6bn just a year earlier and it paid a dividend of 25c per share. It closed the period with a $3.3bn cash balance.

On the same day it released its results, Pilbara Minerals released an updated JORC Mineral Resource for Pilgangoora. It has a total Mineral Resource of 413.8Mt $ 1.15% lithium for 4.8Mt of lithium. Of this 22.1Mt @ 1.34% lithium for 0.3Mt is measured although 315.2Mt @ 1.15% lithium for 3.6Mt is Indicated. The balance of the resource is in the Inferred category.

What about the lithium price

You might say the company is worth investing in given lithium demand. But of course, past performance is not a reliable indicator of future performance. In addition, lithium prices are retreating from all time highs. Just look at Pilbara’s most recent quarterly update – the average realised sales price was US$2,240 per tonne, down 47% from 12 months ago. Lithium sales came in 6% higher than 12 months ago, at 138.2kt, although unit operating costs from Port Headland were 18% higher than the year before.

Consensus estimates look promising

Consensus estimates for FY24 expect $1.7bn in revenue and a $631m profit. Most companies would die for these sort of figures, unless of course they were over 50% retreats from 12 months ago like these ones would be. There are 18 analysts covering Pilbara and the mean price is $4.08 per share, barely 10c higher than the current price. At the same time, it is trading at just 8.8x EV/EBITDA and 16.1x P/E for FY24, so you might say it is compelling on this basis alone.

Perhaps FY24 will just be a one-off dip and growth will return in FY25. Analysts expect this, although it will be several years before revenue and earnings return to FY23 figures – in fact, these are not expected over the 10-year horizon analysts have forecasted. Analysts expect 10% revenue growth and 5% profit growth in FY25, followed by 34% revenue growth and 40% profit growth in FY26. Nonetheless, the projected FY26 profit is 40% lower than FY23 and earnings are barely half of FY23.

So, should I invest in Pilbara Minerals now?

It’s clear lithium is a great space to be in right now and will be for some time to come. But the question of which company you invest in comes down to your risk appetite and whether or not you believe that investors will tolerate a ‘new normal’ for the lithium market.

If you like diversification, other stocks could be better such as Mineral Resources. But for investors with long-term patience, it might be worth holding this one even if the short-term is volatile (or perhaps even quiet).

What are the Best ASX Stocks to invest in right now?