A hidden deep tech portfolio with a free option on growth

Powerhouse Ventures (ASX:PVL) is an A$18.6 million deep tech portfolio that most investors have not noticed yet.

PVL is now rebuilding itself around a deep tech portfolio growing at 30% per half, an advisory business starting to scale, and a new fund that could re-rate the company if it attracts external capital.

The market is already valuing PVL close to its portfolio net tangible assets (NTA). That means the advisory business and Powerhouse Fund are effectively being priced at zero.

For investors, this creates a potential high-upside deep tech opportunity, but it is still early.

Before looking at the investment thesis, it is worth understanding PVL’s history and what the board is trying to change.

What Is Powerhouse Ventures, and What Changed?

Powerhouse Ventures may be a new name to some readers.

Historically, the company was a classic ASX-listed venture capital investor. It invested in early-stage deep tech companies, waited for those businesses to mature, and generated returns when portfolio valuations moved higher.

The problem was that revenue was lumpy. Earnings relied heavily on investment gains, rather than a more consistent base of earned income.

The core shift today is that Powerhouse is being rebuilt around two pillars, new people and platform.

The people piece matters because this is the core driving factor of the success of the rebuild. The board now brings deeper commercial relationships and experience across capital markets, corporate advisory, funds management, and next-generation technology.

New Leadership Reshapes the Powerhouse Story

James Kruger (Far Left) is a seasoned executive and investment banker, with more than 20 years at Macquarie Group in senior roles across commodities, derivatives, investment banking, funds structuring, and group-wide strategy.

He is also a long-time investor in quantum computing, materials science, and other frontier technologies.

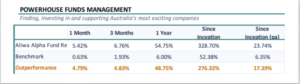

Dave McNamee (Middle) is the founder and Portfolio Manager of Aliwa Funds Management, a boutique investment firm focused on finding, investing in, and supporting Australia’s best emerging companies.

His role has naturally extended into working closely with boards and management teams on execution, strategy, and capital markets initiatives.

Doron Eldar (Far right) is a tech entrepreneur and venture capitalist with more than a decade of senior leadership experience across both sides of the industry. He is a Partner at SIBF, an Israeli venture capital firm, with expertise across corporate strategy, business development, M&A, and go-to-market execution.

Investors can see the common theme. The board has deep experience in technology, but each member also brings complementary skills across capital markets, advisory, funds management, M&A, and business development.

That mix matters because Powerhouse is no longer just a passive investor in early-stage technology companies. With new leadership in place, the company now has a clearer mandate to grow its fund management and corporate advisory segments.

The Three Pillars of the New PVL

Now with a new team, the second major pivot is the business model.

The company is retaining its legacy portfolio of ASX microcaps and unlisted deep tech ventures, which can still generate investment returns.

The advisory side of the business provides corporate strategy, capital raising, and commercial support for ASX-listed and private companies. It earns mandate fees, success fees, and brokerage revenue. In the latest half, advisory revenue reached A$1.92 million, making it the clearest early driver of the new Powerhouse model.

Funds management is newer, but also important. This segment manages investment funds for wholesale clients, giving Powerhouse another pathway to build recurring fee-based income.

It earns management and performance fees, with revenue of A$215k this half. It is still early, but it gives Powerhouse another pathway to build recurring, fee-based income.

But the key difference with the shift in the business model is that Powerhouse is no longer just waiting for portfolio revaluations. It is building an operating platform around advisory, funds management, and capital markets execution.

All steady cash flow, which gives investors clearer visibility of the company’s profitability profile as the business model matures.

Powerhouse Advisory Returns

Powerhouse Funds Management Returns

Powerhouse Starts Building a More Repeatable Earnings Base

Here is where the story becomes more interesting. The right changes are already showing up in the numbers.

In H1 FY25, Powerhouse Ventures generated A$3.6 million in total revenue. Most of that came from A$3.2 million in investment gains, while earned fees were just A$290k.

In H1 FY26, total revenue increased 27% to A$4.6 million. But the number investors should focus on is earned fees, which jumped 647% to A$2.1 million.

That is the early proof point. Powerhouse is starting to build the fee-earning revenue base it has been talking about, and this revenue should be higher quality, higher margin, and more repeatable than investment gains.

So management is already demonstrating to investors that they are focusing on change.

The old Powerhouse made money by holding investments and waiting for valuations to move. The new Powerhouse is spending money to build a corporate advisory and funds management platform.

That makes short-term profit look weaker, but it improves the long-term quality and predictability of earnings.

Net profit fell 47% to A$1.14 million. On the surface, that looks disappointing. But the prior period benefited from larger investment gains of A$3.29 million versus A$2.41 million this half, and almost no advisory cost base.

This half was different. The advisory business is now staffed and operational, which drove employee costs higher from A$249k to A$2.07 million. But that headline increases needs context. Around A$1.05 million related to share-based payments issued to the team, which is a non-cash expense. A further A$383k in share-based payments was accrued as part of the earnout fee payable to the vendors of Aliwa. That was the biggest driver of the profit decline.

The Investors’ Takeaway for Powerhouse Ventures

We will be covering Powerhouse Ventures more closely from here.

At an A$18 million market cap, Powerhouse is still in an early-stage transition. At A$0.115 per share, the stock trades roughly in line with its audited NTA of A$0.119 per share, meaning investors are effectively paying for the portfolio and getting the advisory and funds management platform for free.

The H1 FY26 result looked messy on the surface, with profit down and costs up. But those costs reflect a business being rebuilt.

The key shift is advisory revenue. Fees reached A$2.17 million this half, up from just A$291k a year ago.

The model is use deep tech expertise to win advisory mandates, take fees in cash and scrip, launch a venture fund for external capital, and build recurring management fees over time.

The investment case now comes down to execution. If management scales the advisory pipeline and launches the fund, the market has a reason to take another look.