Investment Case Summary

- Insiders and the major shareholder have already committed roughly 80% of the A$3.84m raise.

- Nearly a third of proceeds fund working capital, hinting Al Wash-hi Majaza cash flow is still ramping.

- FY27 drilling at Block 22B, Block 8 and Daris now has to justify the dilution.

A third of the proceeds funds working capital, not exploration, which tells its own Oman story

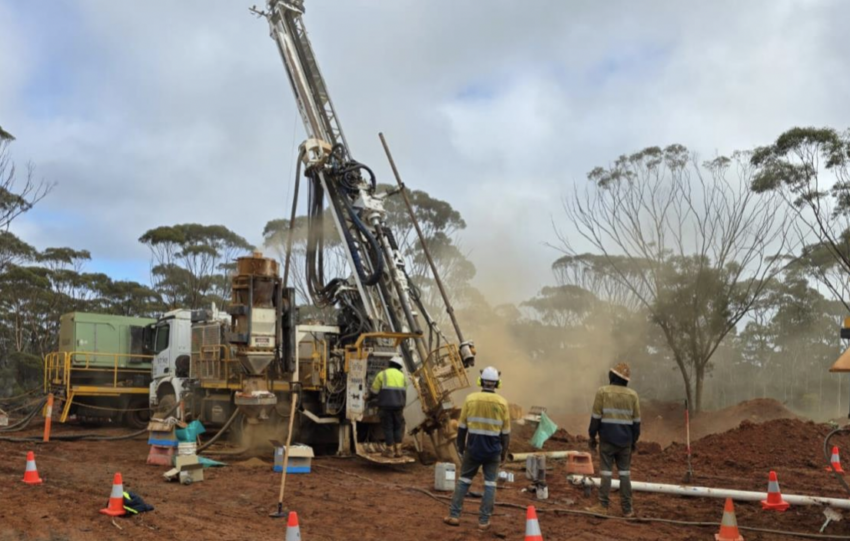

Alara Resources (ASX:AUQ) has come to the market for a modest A$3.84 million through a 3-for-20 non-renounceable entitlement offer priced at 3.2 cents per share. The pure-play copper producer, which operates the Al Wash-hi Majaza copper mine in Oman, will direct the bulk of proceeds toward ongoing exploration at three of its Omani ophiolite tenements.

The number worth noting is not the A$3.84 million headline. It is the roughly A$3.1 million already committed by insiders and the major shareholder before the offer even opens on 16 July 2026.

Major shareholder Al Tasnim Infrastructure has partially underwritten up to A$1.6 million. Director Vikas Jain and his associates have committed A$1.5 million, and Managing Director Atmavireshwar Sthapak adds another A$75,000. That is roughly 80% of the raise essentially spoken for, which tells us this is less a market test and more a routine top-up ring-fenced by the people closest to the story.

Where the money actually goes tells the real story

The use of funds table is instructive. A$2.35 million or 61.3% of the raise goes to ongoing exploration at Block 22B, Block 8 and the Daris project. A further 32.3% is earmarked for general working capital and administrative expenses, with the remaining 6.4% covering offer costs.

That working capital slice is the number that raises an eyebrow. Nearly a third of a raise going to keep the lights on suggests operating cash flow from Al Wash-hi Majaza is not yet doing the heavy lifting investors might expect from a producing copper mine.

For a self-described pure-play copper producer, the ideal would be exploration funded from mine cash flow with equity reserved for growth. The current mix indicates the producer side of the story is still building toward that scale.

Insider commitments are a vote of confidence, and also a warning

The A$3.1 million of insider participation is genuinely supportive. When directors and the major shareholder step up at 3.2 cents, they are backing the ophiolite exploration thesis with their own capital.

The skeptical read is different. When insiders end up doing most of the lifting, it often reflects limited institutional appetite at the current price. Retail shareholders taking their entitlement are co-investing alongside the people who already control the register, which is fine only if exploration results actually land.

What FY27 exploration needs to deliver

Executive Chair Peter Lee framed the raise as funding exciting exploration plans across FY27. With A$2.35 million spread across three projects, drilling budgets will be tight and news flow will need to be efficient.

The most watched programs will be Block 22B and Block 8, both sitting in the same Omani ophiolite terrain that hosts the Al Wash-hi Majaza mine. The dilution math is straightforward, with up to 120 million new shares lifting the share count by roughly 15%.

The Investors Takeaway for Alara Resources

This raise buys Alara another year of exploration and working capital cover, backstopped almost entirely by people who cannot easily walk away. That is a stable outcome, but stability is not the same as momentum. Exploration results from Block 22B, Block 8 and Daris now need to justify the A$2.35 million spend, and Al Wash-hi Majaza needs to reduce the reliance on equity for basic working capital.

Our concern is that if FY27 exploration does not produce a clear catalyst, the next capital conversation will start from a lower base. The general meeting on 7 August 2026 is the first real checkpoint. For readers who want the fuller history on this name, our previous coverage sits at stocksdownunder.