Beacon Lighting (ASX:BLX) flies under many investors’ radar, but it really shouldn’t. The family-owned company sells lights and fans to retail and trade consumers and is the largest company in its industry. It has a proven track record of growth and has more catalysts to come.

Beacon Lighting’s track record

Beacon Lighting listed in 2014 at 66c a share. It opened its first store in 1967 and slowly expanded over time – owning 71 owned stores, 14 franchised stores and four commercial sales stores by the time it listed in 2014.

The company was founded by Ian Robinson who remains Executive Chairman and his son Glen is now the CEO, having worked for the group since 1994 and having been in the top job since 2013. The company’s mission is ‘to brighten our customers’ lives with exciting products that are environmentally friendly and fashionable through expertise and unparalleled service’.

Since listing, Beacon has not raised a cent in capital and is still 55% owned by the Robinson family. At the time it listed it had $11.5m in net profit and $17.2m EBITDA on sales of $150m. It had consistent 15-20% annual profit growth since 1995. Since listing there has been further expansion. Nearly a decade on, it delivered $323m in sales during FY24, $85m EBITDA and a a $30m NPAT.

Beacon now owns over 120 franchised stores. It has avoided supply chain issues because it is a vertically integrated business that controls its own chain. Thus, its gross profit margin has been over 65% for 5 years now.

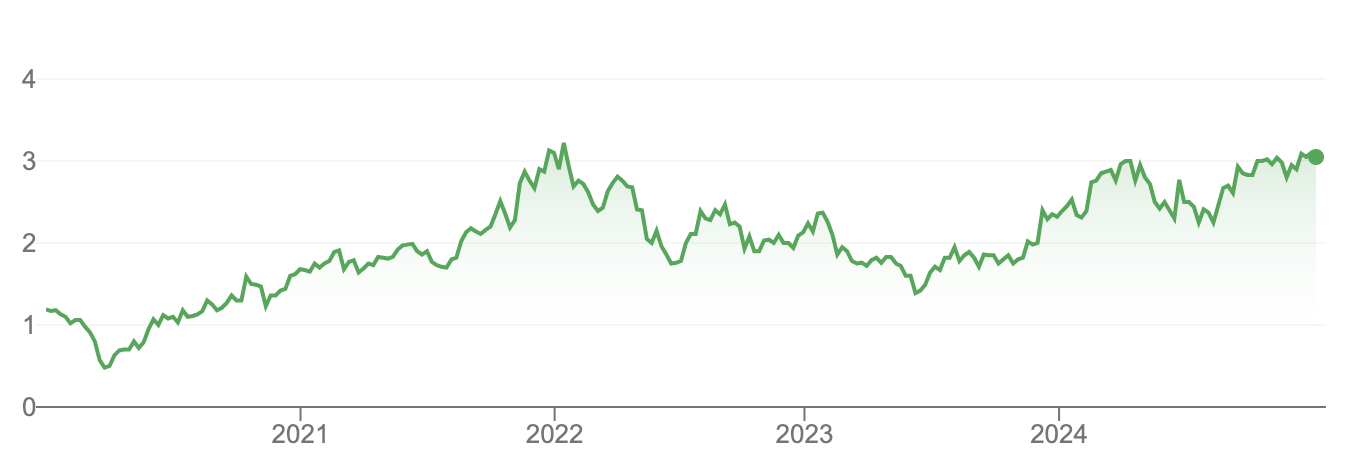

It has a cash balance of $46.2m and relatively modest capex of $9m. On top of all this, it has a loyalty program with 900,000 people (over 3.5% of Australia’s population). BLX shares are up 27% in the last 12 months and over 150% in the last 5 years. It must be doing something right.

So what is next?

We all know that consumers spent more on home improvement products during the pandemic. And this has inflated Beacon’s sales during the COVID years. But, while some companies with inflated sales had them crash back to earth, this has not been the case here. Furthermore, there are several catalysts going forward. Beacon will inevitably continue to generate good results.

In the longer term, the company is hoping to capitalise on broader trends in the lighting industry, like sustainability and energy efficiency. We think the latter will be relevant given the current highs in electricity prices.

We also think that Beacon can continue to expand in Australia and overseas. At home, the company thinks there is potential for over 180 stores based on store network research. And overseas, it has set up showrooms and warehouses in Hong Kong, the Netherlands, Germany, China as well as three in the US to attempt to penetrate the market with its products.

No, you won’t be seeing Beacon branded stores over in the USA, but it will sell into local lighting stores, which tend to be small, family-owned businesses (one example being Lamps Plus) as well as through Ecommerce outlets (Amazon in the US and TMall in China and Hong Kong).

Consensus surprisingly negative

Analysts covering Beacon Lighting aren’t optimistic with a target price of $3.08, roughly in line with the current price. They expect flat EBITDA and NPAT for FY25, but for 4% revenue growth to $336.2m. In FY26, they expect $365.5m revenue (up 9%), $98m EBITDA (up 11%), and a $35.6m profit (up 19%). It has a P/E of 19.8x for FY26, an EV/EBITDA of 8x and PEG of just over 1x. We think this company is a bargain at this price.

So, keep your eye on Beacon Lighting. You may not gain as much than if you bought a micro-cap explorer and it became the next Chalice (ASX:CHN), although it is a solid business that presents far less risk and offers clear upside going forward.

What are the Best ASX Stocks to invest in right now?