Vicinity Centres (ASX:VCX) is one property stock we’ve been keeping our eyes on for several months. Vicinity Centres has some of the most highly coveted, high-lease retail assets in Australia, but is highly reliant on foreign tourists. This led to the business essentially going into limbo for several months.

Even as malls have been permitted to re-open post-pandemic, the company’s share price continued to lag as rising interest rates put a dent in the company’s profits. But with a 29% gain in 12 months, and the company now trading at a premium to its NTA, is it the start of a period of growth?

Who is Vicinity Centres?

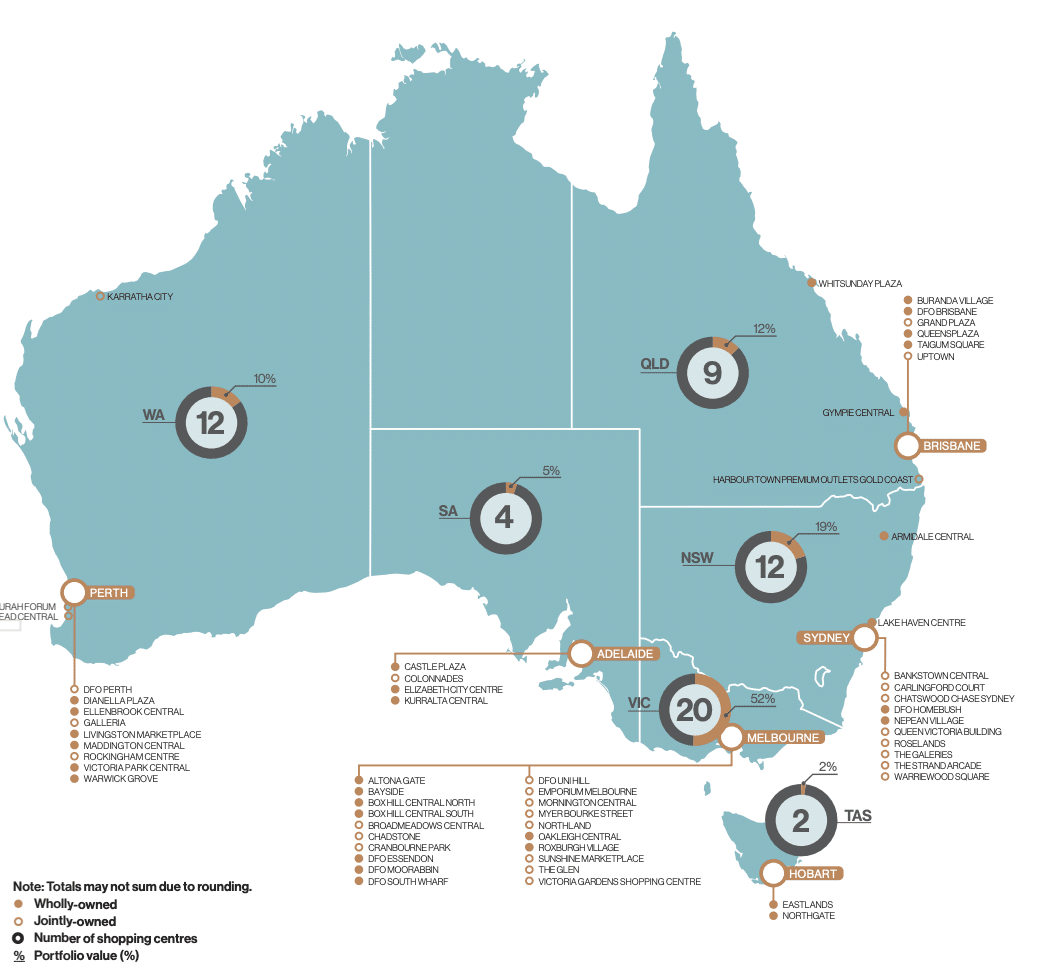

Vicinity Centres is a shopping centre landlord, operating shopping centres and leasing them to tenants. The company was created in 2015 from the merger of Federation Centres and Novion Property Group. It has over 52 shopping centres under management, which receive a cumulative $18bn in sales and 390m customer visits annually.

Vicinity’s $24bn portfolio includes several flagship stores, including Chadstone shopping centre in Melbourne, Queens Plaza in Brisbane and Chatswood Chase in Sydney and corporate offices at certain sites.

The company has a diversified mix with the top 10 tenant groups not accounting for over 23.4%. The biggest is Wesfarmers that accounts for 4.6% (including Kmart, Target, Bunnings and Priceline amongst others) with Woolworths Group (including Woolworths and Big W) and Coles Group (including Coles, Liquorland and Vintage Cellars) making up 6.5% between them, then Myer & Premium Investments’ brands making up 3%. 99.4% of space is occupied and the WALE is 4.3 years by area, 3.6 years by income.

Vicinity copped a massive hit from the pandemic

COVID-19 forced the shutters down on non-essential retail and sent Vicinity swinging from a $346.1m profit in FY19 to a $1.8bn loss in FY20. Although essential retailers in suburban malls mitigated the damage, its CBD assets were hit by people working from home and the elimination of tourism through border closures. The company undertook a $1.2bn capital raising in the early months of the pandemic and wrote down $1.79bn from its portfolio.

In FY21, Vicinity still made a statutory net loss but only $258.0m. Snap lockdowns impacted store trading and visitor numbers, but visitation numbers quickly returned whenever restrictions were lifted. In every quarter of FY21, visitor numbers at stores excluding Victoria and CBD assets in all states were above 90%, and retail sales were above 2019 levels. Vicinity’s Victorian assets suffered more time in lockdown than any other Australian state and even without lockdowns, CBD flagship stores were impacted by an absence of tourists and office workers.

Nevertheless, by the second half of FY21, retail sales across the entire portfolio were under 4% below pre-COVID levels and visitation numbers at over 75%.

A slow recovery and even slower shareholder response

Let’s fast forward to FY22, a period that included the Delta Lockdowns and the Omicron wave but also included the re-opening of Australia’s international borders. The company returned to NPAT profitability, making $1.2bn. Its FFO came in at $598.1m, or 13.1cps, and it paid a distribution of 10.4c, representing a 95.3% payout of Adjusted FFO. So, the only way from here was up, right? Well, yes and no as the share price continued to lag.

You see, even though shoppers returned to suburban malls, the company’s flagship malls in the CBD that relied on international tourists and office workers were slower to recover. Adding insult to injury was the rapid rise in interest rates that hit property valuations. And so its NPAT in FY23 was was just $271.5m, despite FFO being over $80m higher, at $684.4m (or 15c per share). It paid 12c per share to its investors.

FY24 saw its profit improve to $547.1m and it made $492.6m in 1H25. The company has guided to FFO of 14.5-14.8c for the full FY25, compared to 14.6c in the year before. FY24 saw the company undertake 7 strategic asset sales and smaller developments including a new office tower to host the corporate offices of Kmart and Adairs (among others). In 1H25, the company confirmed it was on track to reach its guidance, and the company confirmed a few weeks ago promised it would hit the top end of its guidance.

The company has undertaken a number of renovation projects including The Market Pavilion at Chadstone – essentially a new food court. It attracted more visitors on the first day than the entire 2024 Black Friday and Black Saturday. Its new One Middle Road tower at Chadstone, which will become the office of Adairs and Kmart (among others), is on track. And it completed the divestment of a number of properties including Roselands and Carlingford Court. A major renovation at Chatswood Chase remains on track to open by the end of this calendar year (i.e. 2Q FY26).

Something fascinating the ocmpany did in its recent update was breaking down sales by product category. Leisure was the highest, up 10% in the 6 months to March 31, 2025. Retail services, food retail and homewares was up 6%. The most disappointing was mobile phones which was down 0.4%, then general retail that only gained 0.1% and footwear was up 1.1%.

There is hope now

Vicinity’s NTA stood at $2.39 per share and now the company is finally back to trading at a premium to its NTA. The company is not yet back to its pre-COVID levels, but is very close to it. It is inevitable that the threshold will be crossed in the coming months.

As long as Vicinity meets its FY25 guidance, we think investors will do well out of this one in the coming months.

What are the Best ASX Stocks to invest in right now?