2 years since Block shares listed on the ASX: Can it boost to new heights in 2024?

![]() Nick Sundich, April 9, 2024

Nick Sundich, April 9, 2024

The Afterpay acquisition was not just noteworthy because it was the biggest corporate takeover in Australian history, but also because Block shares listed on the ASX rather than just snapping up Afterpay shares and never to be heard from again.

Although shares in the Jack Dorsey-founded company have been underwater for most of its listed tenure due to the Tech Wreck, they have been trending upwards in recent months. So is it time to get in?

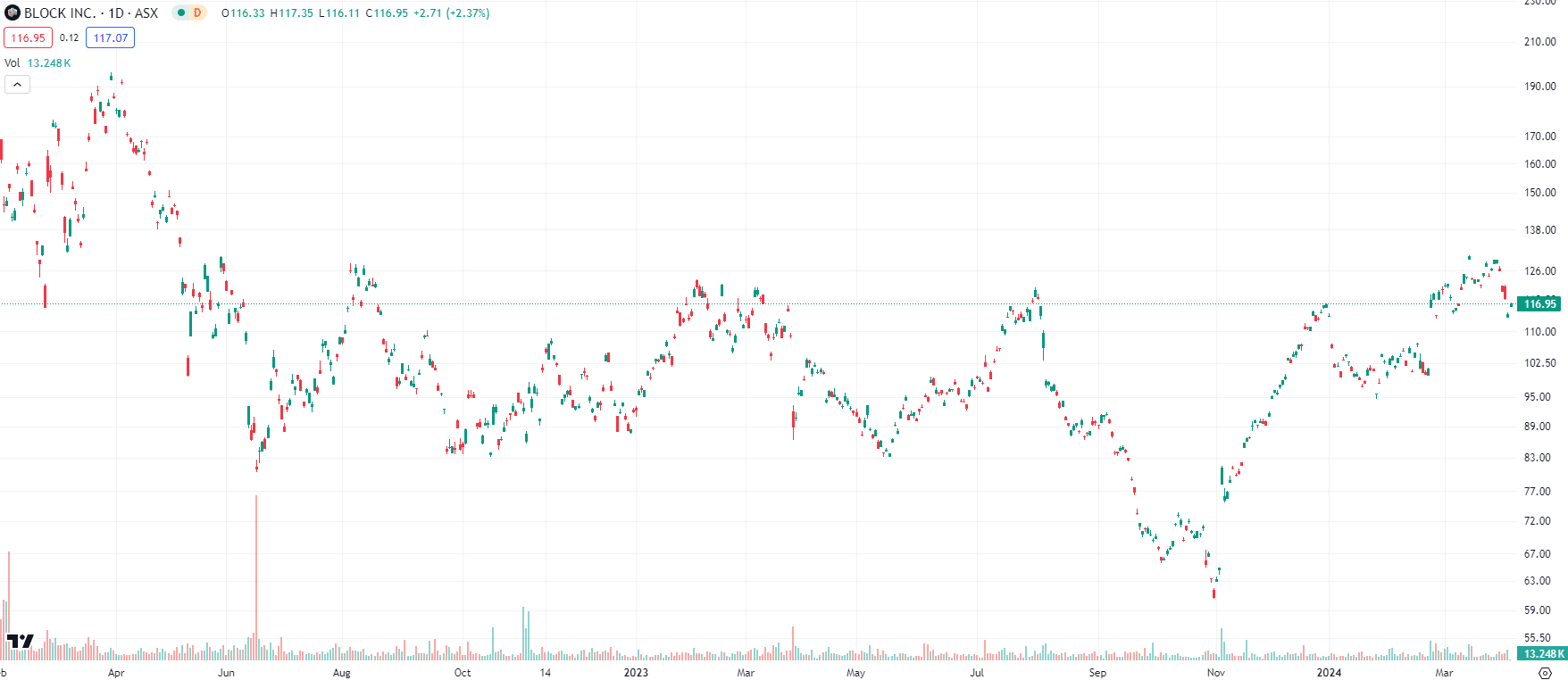

Block (ASX:SQ2) share price chart, log scale (Source: TradingView)

Why are Block shares listed on the ASX?

Because, as noted above, it acquired Afterpay. And the deal was paid in its own shares rather than cash, because it lacked the cash reserves to pay in that way.

Block shares on the ASX are listed as CDIs (Chess Depository Indices), as are most of the US companies with dual listings on the ASX. Unlike many others, Block CDIs are strictly 1:1 – 1 CDI represents 1 ordinary share in the company.

Who is Block?

Block is a US fintech, formerly known as Square, founded by Jack Dorsey in 2009. Dorsey founded Twitter just 3 years earlier, but was inspired to start Block after a friend of his couldn’t complete a $2,000 sale of glass faucets and fittings because the other party could not accept credit cards.

Block has two main parts to its business. Its Seller business manages payments and lends money to merchants and its Cash App that allows consumers to transfer, spend and invest money. The latter has over 50m Monthly Active Users while the former is used by over 30% of US small businesses.

One App to rule them all?

In buying Afterpay, Block made Afterpay as a payment method in both apps. Block has also made forays into crypto, with a business called TBD that is focused on creating crypto developer tools. Its Cash App also supports bitcoin. Finally, it owns Tidal, a music streaming platform founded by Jay-Z. The jury is still out on how it fits into the company’s boarder business strategy.

The company has benefited from the shift of transactions from physical cash into the digital world. It generated US$228bn in Gross Payment Volume in 2023.

Growth ahead?

The company purports to have penetrated less than 5% of its market and that the market keeps expanding. It claims that there is a US$75bn opportunity for the Cash App and $130bn for the Business Division (which it calls Square). The Cash App is predominantly used by Millennials and Gen Z, although it is only 34% and 25% penetrated in those demographics.

Unfortunately, the Tech Wreck has meant that investors have gone cold on ‘growth at any cost’ companies, in other words, companies that are not profitable.

In FY23 (which is the calendar year), the company made $21.9bn in net revenue (up from $17.5bn the year before). The company’s made an overall net loss of US$21bn but this figure is $9.8bn when the amount attributable to non-controlling interest is excluded.

2024 is looking solid

This year, the company is expecting a full-year profit of over US$200m and EBITDA of at least $2.6bn. This is driven not only by growth at the top line, but reductions in the bottom line. Block has sought to cut costs, laying off 10% of its workforce at the start of this year.

Analysts covering the company in the US (who total 43) agree and forecast ~10% revenue growth, as well as a 12-month share price target of US$89.45 per share, up 15% from the current share price. Aussie investors aren’t as optimistic and have a mean target price of A$101.04 per CDI, down from the A$116.88 it is right now. We think its US shares are worth US$117.59 per share, up nearly 50% from the current price, on the basis of our DCF models on the company, using consensus estimates and a 9.9% WACC.

Block is one to watch

If Block can be profitable in CY24, we are confident that both its US shares and CDIs will rerate. Thankfully, investors shouldn’t have to wait another 12 months to see – they should be able to see evidence that the company is on track each quarter, starting with its next quarterly results release, due in early May.

We think investors need only look at the example of Life360 (ASX:360) to show that US-headquartered companies on the ASX can re-rate if they can deliver profitable growth.

What are the Best ASX Stocks to invest in right now?

Check our buy/sell tips

Blog Categories

Get Our Top 5 ASX Stocks for FY25

Recent Posts

Your invitation to the Freelancer Investor Day

Your invitation to the Freelancer Investor Day Freelancer (ASX: FLN) is a Sydney-based company that has been the subject of…

Kamala Harris stocks: If Joe Biden’s VP wins the White House in 2024, which stocks will win?

With the US Presidential election now certain to be a Kamala Harris v Donald Trump showdown, we’ve looked at so-called…

South32 (ASX:S32): Is it the dark horse amongst ASX 200 miners or have cyclones and commodity prices hit it too hard?

South32 (ASX:S32) began life as a spinoff from BHP back in 2015, capitalised at $9bn. In mid-2024, it is capped…