Flight Centre (ASX:FLT)

SELL Flight Centre (ASX:FLT), 23 February 2023

Our subscribers have made 24.2% on our original call on Flight Centre (ASX:FLT). It is time to take profits.

While FLT is up 24.2% from 6 October (when it was $14.87) we now think it is worthwhile to take some profits on this one.

Flight Centre (ASX:FLT) share price chart, log scale (Source: TradingView)

FLT records positive 1HY23 results

As with Air New Zealand (ASX:AIZ), we think investors will be pleased with its results, which were unveiled to the market yesterday (22 February)

Flight Centre’s Total Transaction Value (TTV) came in at $9.9bn, which was up 203% from 12 months ago and 80% of 1HY20 (the last 6 month period unaffected by the pandemic.

Underlying EBITDA came in at $95m. This was 19% above the mid-point of the initial 1HY23 guidance the company provided shareholders and represents a $280m turnaround from 12 months ago.

But its time to take profits

We believe that, ultimately, the travel thematic has run its course and that there are better opportunities elsewhere.

We concede that Flight Centre has more potential to derive incremental shareholder value from here compared to Air New Zealand.

This is for two reasons. First, it has greater exposure to the re-opening of China than Air New Zealand. And second, last month’s acquisition of luxury travel agency Scott Dunn has given it exposure to the luxury travel segment that will be unaffected even if the global economy enters a recession. We also note that unlike Air New Zealand, it will derive a greater proportion of its earnings from 2HY23.

We are concerned about a number of headwinds, most particularly the potential for air fares to drop – hence eating into their margins. Bear in mind that many airlines have slashed the commissions they pay to travel agents since the pandemic. FLT has also hinted at M&A activity which could dilute shareholders, eat into its cash reserves, or both.

Ultimately, we think it is time to take profits on this one, given the returns that we have derived in the 4 and a half months since we opened this position.

——————————————————————————————————————————————————–

FYI, Our original investment strategy for Flight Centre (ASX:FLT) dated 6 October 2022

Our investment strategy for Flight Centre (ASX:FLT)

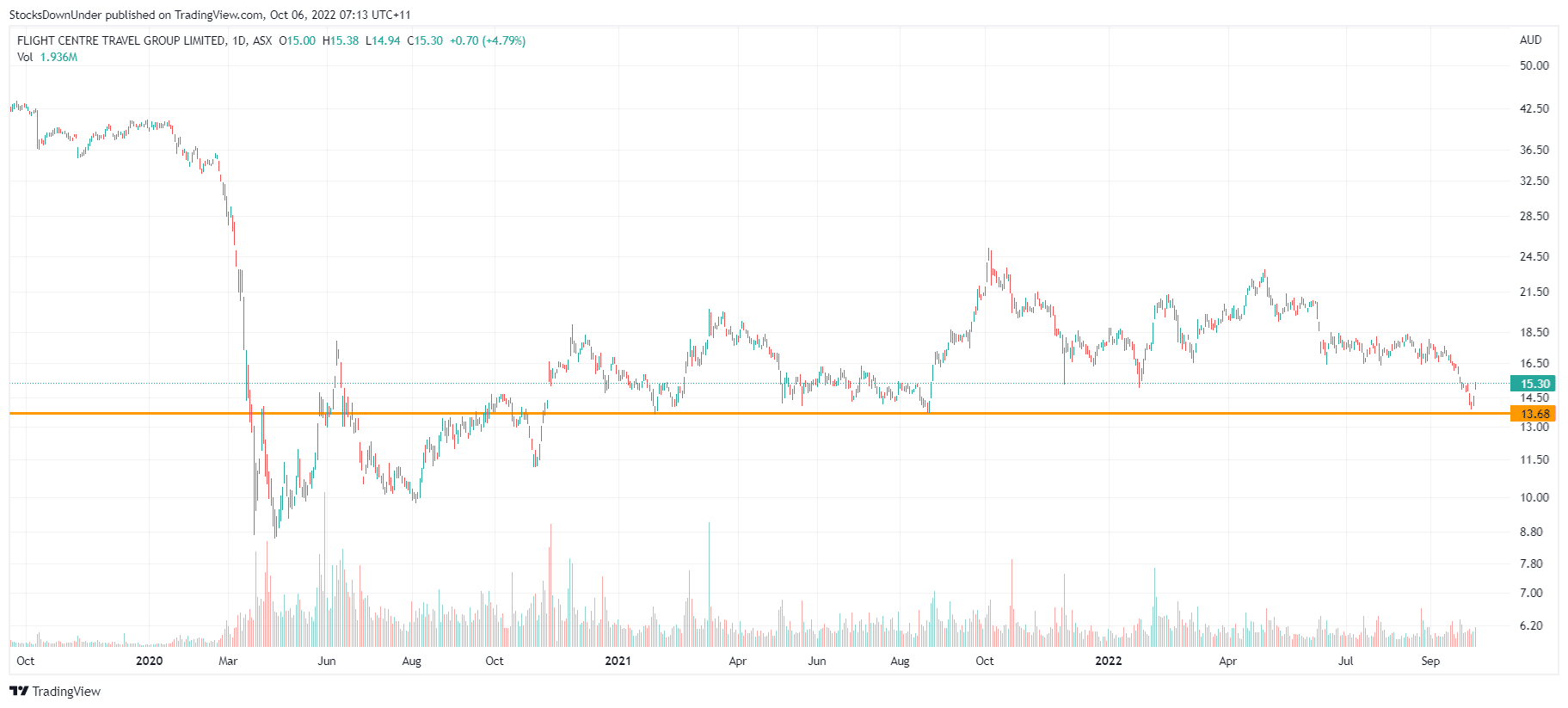

- Buy Flight Centre up to $15.30.

- Our minimum target price for FLT is $18.25.

- Use a stop loss at $13.80.

Check out our recent interview on AusBiz about Flight Centre here.

Who is Flight Centre?

Flight Centre is a Brisbane-based travel company. Since the early 1980s the company has evolved from the core Flight Centre travel agency brand in Australia into multiple travel operations around the world. Today the company has over 40 brands that sit within the leisure, corporate and wholesale travel industries.

The company has grown into the sixth largest travel company in the world and the first not to be headquartered in the United States.

The company’s founder and major shareholder Graeme Turner remains in charge forty years on as CEO and is widely regarded as one of Australia’s more talented business leaders.

FLT’s share price has performed very well in the light of the 95 cents per share IPO price from late 1995. The all-time high for the share price was 20 August 2018 at $69.36.

Our investment thesis for Flight Centre:

- Flight Centre benefits from current strong demand for travel. We argue that people’s historic desire to travel more hasn’t been slaked. Indeed, it has been fuelled by the two years of being locked down.

- This company has a long track record of growth, beginning with a single Flight Centre travel agency back in Brisbane in 1982.

- The company usually gets on the ‘right side of history’ in terms of trends in the travel industry, most notably in its recent move into business travel. Also, a talented management team has been able to weather a number of downturns in the travel industry, like after the first Gulf War in 1991.

- Flight Centre is ‘high tech / high touch’. While the Internet has led to the rise of the online travel agency, Flight Centre has carved out a solid and enduring niche in personalised service in its core Flight Centre agencies, while also growing with its online offerings.

- The FY22 result was better than Flight Centre initially expected and in 2HY22 the company was back in the black. Impressively, Flight Centre was profitable for the whole of FY22 for its corporate business and also for its EMEA business. The last four months of FY22 saw a return to profitability in Flight Centre’s Australia and New Zealand business.

- Gross Total Travel Value (TTV) was higher than pre-pandemic in the month of June 2022, indicating that Flight Centre is now, more or less, back to normal.

- Flight Centre can be expected to enjoy two very strong years of growth as indicated by the consensus numbers we show below.

- The company benefits from the current complexities around travel, where there are concerns by travellers around cancelled flights, lost luggage and potential border-crossing issues. In this kind of environment people prefer to deal with a real person rather than an online interface.

- It is managing its brand and appeal to potential employees well as indicated by the high number of applicants applying for new positions.

- FLT expects to be doing better at capturing online business over the next few years and not just through the foundation Flight Centre brand, but also through other brands such as StudentUniverse, acquired by Flight Centre in 2015.

- The balance sheet is in good shape with A$1.3bn in cash and investments on hand as at June 2022 balanced against only $350m in bank debt. Some investors who are negative on the story will point out that Flight Centre issued $800m in convertible notes in 2020 and 2021, and these notes convert at any time. However, the first $400m convert at $20.04 and the other $400m at $27.30.

Flight Centre price chart, log scale (Source: TradingView)

Why has Flight Centre stock declined between late April 2022 and early October?

- The stock has been heavily shorted in recent weeks. The stock is about 15.6% shorted currently, making it the most shorted stock in the ASX200. While concerning, this high number suggests that a solid turnaround in the Flight Centre business can be accompanied by short covering, which would propel the story higher.

- The short sellers expect FLT to be impacted by an economic slowdown, which is likely to be coming in Australia and around the world as central banks raise interest rates to fight inflation. We argue that, even if the economy slows slightly, Flight Centre will still benefit from the high need people have to travel in the post-pandemic environment.

- Some investors will have been annoyed by the pandemic recapitalisation that Flight Centre went through to stay alive in a period where there was not much travel to book. The company raised ~$700 million in April 2020 in a $282m placement and 1-for-1.74 accelerated pro rata non-renounceable entitlement offer at $7.20 per share. We argue that the recapitalisation is ‘ancient history’ as far as the forward outlook is concerned.

- The full recovery won’t be in place until FY24, with travel still moving towards normal through FY23. Flight Centre lost money in FY22 (obviously) and only returned to the black in the second half. That will have left some investors wary.

- Flight Centre hasn’t offered FY23 guidance, so we likely won’t find out until close to the end of calendar 2022 or into early 2023 just how well the company is doing in this recovery.

- There are concerns about margins since Flight Centre, like every business around the world, is not immune to cost increases. We argue that a rising top line for Flight Centre more than makes up for these issues.

- There are concerns about Qantas’ recent decision to sell airfares exclusively through its own channel, which it can now do more easily thanks to New Distribution Capability (NDC), an IATA standard to allow the systems of all travel players to talk the same technical language. However, Flight Centre has already anticipated how NDC will change the game. In March 2022 it moved to 70% of TPConnects Technologies, a Dubai-based business that is an NDC-certified IT provider and aggregator.

$18.25 is a reasonable initial price target

- The stock was trading at that level as recently as mid-August 2022.

- FLT is currently trading at an EV/EBITDA multiple of 11.3x for FY23 and 7.4x for FY24, which we believe is very attractive given the expected EBITDA growth of 53% in FY24 following a return to EBITDA positive in the current financial year (a $485m EBITDA swing from -$183m in FY22 to $302m in FY23).

- Our secondary target is $21.00.

Catalysts for the re-rate of Flight Centre

We see four main catalysts to prompt a re-rating of the stock:

- Ongoing recovery of global travel numbers as airlines get their operational issues under control.

- Data on inbound and outbound tourism in Australia, which is reported monthly by the Australian Bureau of Statistics[1]. We believe the data will show a positive trend on a return to regular travel.

- The half-yearly result in February 2023, which we expect can show that Flight Centre is delivering on its recovery plans.

- Improving stock market sentiment as the market revaluation, driven by interest rate hikes globally, may soon come to an end. We believe inflation expectations for 2023 may have peaked recently, which should result in slower than previously expected interest rate hikes going forward.

Risks

- A loss of market share in travel;

- A decline in the traditional brick and mortar travel agency as travellers move more towards online offerings;

- Slowness of business travel to resume with travellers preferring to wait until the airlines are functioning normally.

- Difficulties in finding good staff in an environment of very low unemployment;

- Other cost increases in a generally inflationary environment;

- Missed guidance as we move towards the 1H23 result.

Update 14 November 2022

Following the company’s solid share price run since inclusion into Concierge, we increased our stop loss level from $13.80 to $15.50.

[1] https://www.abs.gov.au/statistics/industry/tourism-and-transport/overseas-arrivals-and-departures-australia.