Bubs Australia (ASX:BUB): One of the few infant formula stocks building a post-China future

![]() Nick Sundich, September 18, 2024

Nick Sundich, September 18, 2024

Bubs Australia (ASX:BUB) just might have a future beyond China. After the pandemic shut down the infant formula trade, companies that had previously been reliant on China sought other markets in the ASEAN region such as Vietnam. An infant formula shortage in the USA in 2022 led to a number of stocks, led by A2 Milk, entering the market on a temporary basis with hope it could become permanent. Bubs has been one company that has persisted, and the persistence might pay off.

History of Bubs Australia

Bubs Australia listed in early 2017 from the shell of Hillcrest Litigation Services. It came to the ASX having been in business for over a decade before not just offering infant formula but organic baby food too. Founder Kirsty Carr had first-hand experience as a mother of three, along with a decade-long stint of living in Asia which included a time as a Communications Strategist for Cathay Pacific. When it listed, the company closed its first trading day at $0.13 per share and a market capitalisation of $32m. It reached an all time high of $1.59 in mid-May 2019, a fall triggered by Kirsty Carr taking some money off the table (in other words, selling shares) to buy a house. Shares went into terminal decline even in spite of major distribution deals into China and Australia – heck, it even had a joint venture partner in China (Beingmate).

Bubs Australia (ASX:BUB) share price chart, log scale (Source: TradingView)

The company pursued alternative markets including Vietnam and Singapore and even though these products were embraced, there just wasn’t the population to derive demand. The only market open to the company was the US, and it launched on a small scale in 2021 on Walmart and Amazon. 2022 provided the opportunity for the company to make its mark with companies such as Bubs given fast-track approval to temporarily sell infant formula in the market. It ended up selling $48.1m in the June quarter of CY22, 278% ahead of 12 months earlier and 174% ahead of the March quarter. It delivered over half a million tins between May and July 2022.

2023 was a difficult year for the company. The company pushed for permanent market access to the USA, but was overshadowed with boardroom turmoil and sales in China being below expectation. Bubs ended up terminating Kirsty Carr and having to eventually pay a settlement to stop her suing the company. A strategic review was launched to try and minimise expenses, and it raised $14m in capital at the end of the year.

2024 was OK…2025 could be better

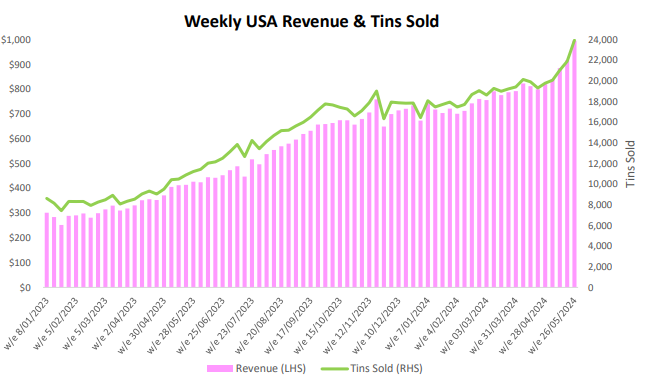

Sales have continued to grow in the USA – its temporary access only expires in October 2025, hence the goal to get permanent approval by then. And Bubs is in the top 6 best-selling infant formula products in the category.

Source: Company

Bubs closed the year with $79.7m in revenue, up 33%, a gross margin of 49%. $35m came from the USA and $17.3m from China, up 46% and 27% respectively. I made $21.6m in Australia, up24% and it has a 52% market share in the goat infant formula market. The company lost $20.9m, but this was only a fifth of the $108.4m loss made in the year before. It holds $17.5m in cash and cash equivalents. For FY25, it has has told investors to expect $102m in revenue and for the company to be breakeven on an EBITDA basis (it made a $19.7m EBITDA loss in FY24).

The key for the company will be ensuring it can maintain permanent access in the USA and it expects approval in October 2025. To this end, it is conducting a clinical trial to demonstrate that babies fed Bubs infant formula grow at the same rate as those fed a commercially available cow milk formula. The most recent update came earlier this week when it reported 400 infants had been enrolled and the trial documentation is expected to be submitted in early 2025.

Conclusion

Bubs has not had the easiest half-decade, but is in a better position compared to other many other companies in its space such as Nuchev (ASX:NUC). It now makes more money from the USA than China and this is very pleasing in our view.

The risk with Bubs Australia is that approval is not extended beyond October 2025 – this would be fatal to the company, although of course this is not the only company with its future contingent on America’s regulators.

What are the Best ASX Stocks to invest in?

Check our buy/sell tips

Blog Categories

Get Our Top 5 ASX Stocks for FY25

Recent Posts

Xero (ASX:XRO) delivered another stellar result in FY25, but is there further upside? Here are 3 reasons why we think it does

Xero (ASX:XRO) is one of the ASX’s best-performing tech stocks over the last decade, offering accounting software helping SMEs do…

Cleanaway Waste Management (ASX:CWY): Is its $5.9bn price right or a load of rubbish?

This week’s Australian stock of the week is Cleanaway Waste Management (ASX:CWY). Capitalised at $6bn, it is Australia’s biggest waste…

Investors are excited about Core Lithium’s planned re-start of Finniss! But here’s why they’re overreacting

Core Lithium’s (ASX:CXO) planned re-start of Finniss has got plenty of investors excited. Shares closed yesterday 35% higher than the…